import pandas as pd import numpy as np import matplotlib as mlb import matplotlib.pyplot as plt import seaborn as sns

In [3]:

stock_data = pd.read_csv(r"C:\Users\HP\Downloads\Copy of Stock_Market_Data.csv") stock_data.head()

Out[3]:

| Date | Name | Open | High | Low | Close | Volume | |

|---|---|---|---|---|---|---|---|

| 0 | 02-01-2022 | 01.Bank | 22.83 | 23.20 | 22.59 | 22.93 | 1842350.41 |

| 1 | 03-01-2022 | 01.Bank | 23.03 | 23.29 | 22.74 | 22.90 | 1664989.63 |

| 2 | 04-01-2022 | 01.Bank | 22.85 | 23.13 | 22.64 | 22.84 | 1354510.97 |

| 3 | 05-01-2022 | 01.Bank | 22.91 | 23.20 | 22.70 | 22.98 | 1564334.81 |

| 4 | 06-01-2022 | 01.Bank | 23.12 | 23.65 | 23.00 | 23.37 | 2586344.19 |

In [8]:

stock_data['Dte']=pd.to_datetime(stock_data['Date'],dayfirst=True) stock_data.dtypes

Out[8]:

Date object Name object Open float64 High float64 Low float64 Close float64 Volume float64 Dte datetime64[ns] dtype: object

In [ ]:

Part1: Data Cleaning and Exploration: # 1. Display basic summary statistics for each column

In [13]:

summary_statistics = stock_data.describe()

print("Summary Statistics:")

print(summary_statistics)

Summary Statistics:

Open High Low Close Volume \

count 49158.000000 49158.000000 49158.000000 49158.000000 4.915800e+04

mean 157.869018 159.588214 155.906364 157.351462 5.619999e+05

min 3.900000 3.900000 3.000000 3.800000 1.000000e+00

25% 19.000000 19.300000 18.700000 19.000000 5.109475e+04

50% 40.300000 41.000000 39.535000 40.100000 1.824160e+05

75% 89.400000 90.500000 87.700000 88.700000 5.401398e+05

max 6000.000000 6050.000000 5975.000000 6000.500000 6.593180e+07

std 520.191624 523.348078 517.136149 519.711667 1.276909e+06

Dte

count 49158

mean 2022-03-31 12:56:37.436836608

min 2022-01-02 00:00:00

25% 2022-02-13 00:00:00

50% 2022-03-30 00:00:00

75% 2022-05-19 00:00:00

max 2022-06-30 00:00:00

std NaN

In [ ]:

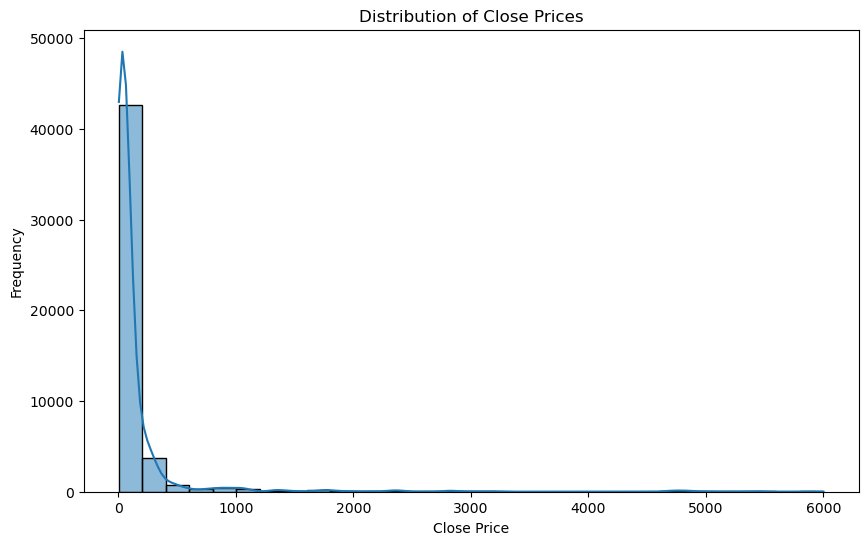

# 2. Explore the distribution of the 'Close' prices over time

In [14]:

plt.figure(figsize=(10, 6))

sns.histplot(data=stock_data, x='Close', bins=30, kde=True)

plt.title('Distribution of Close Prices')

plt.xlabel('Close Price')

plt.ylabel('Frequency')

plt.show()

C:\Users\HP\anaconda3\Lib\site-packages\seaborn\_oldcore.py:1119: FutureWarning: use_inf_as_na option is deprecated and will be removed in a future version. Convert inf values to NaN before operating instead.

with pd.option_context('mode.use_inf_as_na', True):

In [ ]:

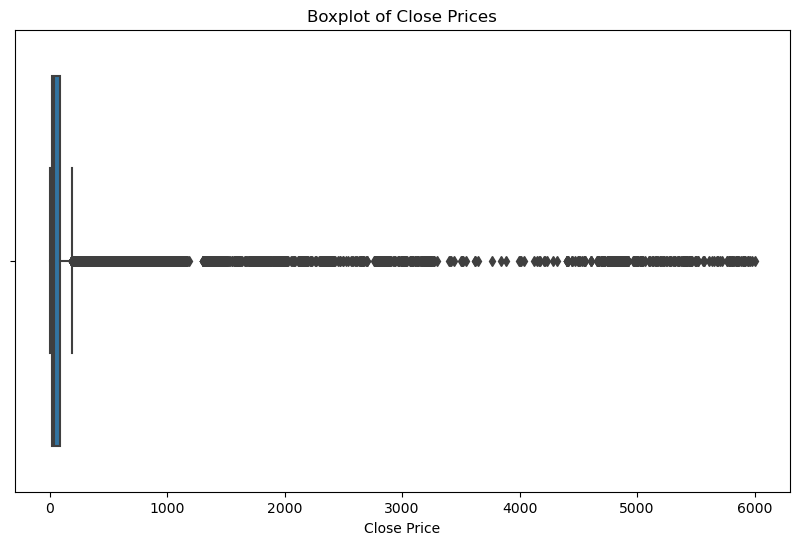

# 3. Identify and analyze any outliers in the dataset

In [15]:

plt.figure(figsize=(10, 6))

sns.boxplot(data=stock_data, x='Close')

plt.title('Boxplot of Close Prices')

plt.xlabel('Close Price')

plt.show()

In [ ]:

# Calculate outliers using IQR method

In [16]:

Q1 = stock_data['Close'].quantile(0.25)

Q3 = stock_data['Close'].quantile(0.75)

IQR = Q3 - Q1

lower_bound = Q1 - 1.5 * IQR

upper_bound = Q3 + 1.5 * IQR

outliers = stock_data[(stock_data['Close'] < lower_bound) | (stock_data['Close'] > upper_bound)]

print("Outliers:")

print(outliers)

Outliers:

Date Name Open High Low Close \

110 02-01-2022 06.Food_&_Allied 303.67 311.01 301.14 305.16

111 03-01-2022 06.Food_&_Allied 309.80 312.41 300.36 303.13

112 04-01-2022 06.Food_&_Allied 305.78 307.39 299.97 303.66

113 05-01-2022 06.Food_&_Allied 305.40 308.92 301.87 303.43

114 06-01-2022 06.Food_&_Allied 303.89 306.60 297.66 299.72

... ... ... ... ... ... ...

49043 26-06-2022 WATACHEM 204.50 211.60 204.50 207.90

49044 27-06-2022 WATACHEM 206.00 209.40 206.00 207.10

49045 28-06-2022 WATACHEM 208.90 210.10 205.00 205.80

49046 29-06-2022 WATACHEM 205.50 210.00 205.40 209.70

49047 30-06-2022 WATACHEM 210.90 215.00 207.70 214.10

Volume Dte

110 187281.15 2022-01-02

111 432190.10 2022-01-03

112 554873.95 2022-01-04

113 617348.90 2022-01-05

114 597532.50 2022-01-06

... ... ...

49043 9785.00 2022-06-26

49044 3714.00 2022-06-27

49045 13759.00 2022-06-28

49046 15023.00 2022-06-29

49047 32851.00 2022-06-30

[6960 rows x 8 columns]

In [ ]:

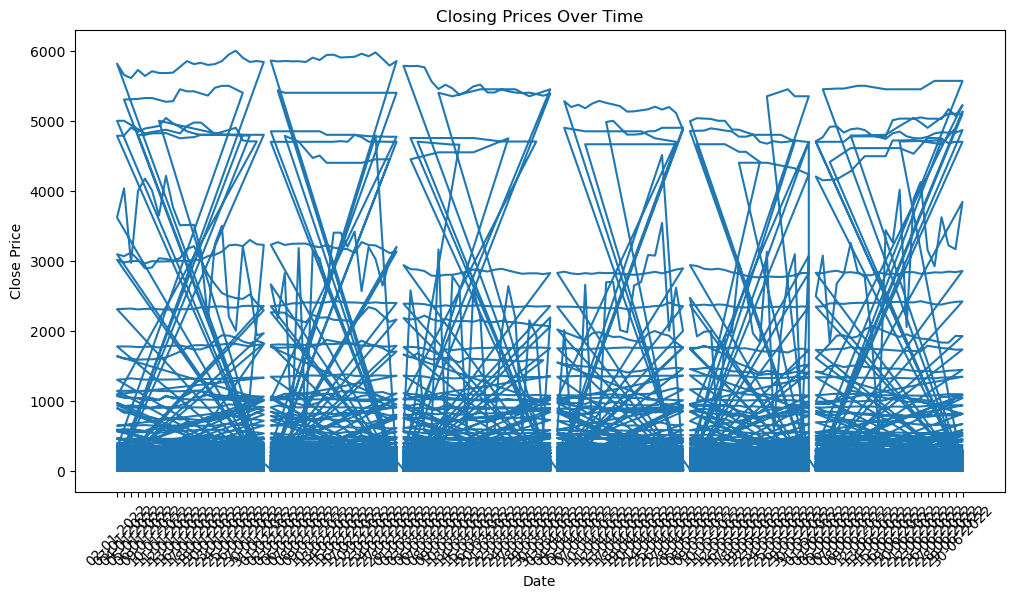

Part 2: Time Series Analysis / Rolling Window / Moving Averages: # 1. # Create a line chart to visualize the 'Close' prices over time

In [19]:

plt.figure(figsize=(12, 6))

plt.plot(stock_data['Date'], stock_data['Close'])

plt.title('Closing Prices Over Time')

plt.xlabel('Date')

plt.ylabel('Close Price')

plt.xticks(rotation=45)

plt.show()

In [ ]:

# 2. Calculate and plot the daily percentage change in closing prices

In [20]:

stock_data['Daily_Return'] = stock_data['Close'].pct_change()

plt.figure(figsize=(12, 6))

plt.plot(stock_data['Date'], stock_data['Daily_Return'])

plt.title('Daily Percentage Change in Closing Prices')

plt.xlabel('Date')

plt.ylabel('Percentage Change')

plt.xticks(rotation=45)

plt.show()

In [ ]:

# 4. Apply moving averages to smooth the time series data in 15/30 day intervals against the original graph

In [21]:

stock_data['MA_15'] = stock_data['Close'].rolling(window=15).mean()

stock_data['MA_30'] = stock_data['Close'].rolling(window=30).mean()

plt.figure(figsize=(12, 6))

plt.plot(stock_data['Date'], stock_data['Close'], label='Original')

plt.plot(stock_data['Date'], stock_data['MA_15'], label='MA 15 Days')

plt.plot(stock_data['Date'], stock_data['MA_30'], label='MA 30 Days')

plt.title('Moving Averages')

plt.xlabel('Date')

plt.ylabel('Close Price')

plt.legend()

plt.xticks(rotation=45)

plt.show()

In [ ]:

# 5. Calculate the average closing price for each stock

In [29]:

print(stock_data.columns)

Index(['Date', 'Name', 'Open', 'High', 'Low', 'Close', 'Volume', 'Dte',

'Daily_Return', 'MA_15', 'MA_30'],

dtype='object')

In [35]:

average_closing_price = stock_data.groupby('Name')['Close'].mean()

print("Average Closing Price for Each Name:")

print(average_closing_price)

Average Closing Price for Each Name:

Name

01.Bank 21.260902

02.Cement 96.600820

03.Ceramics_Sector 71.225164

04.Engineering 132.352459

05.Financial_Institutions 29.253525

...

WMSHIPYARD 12.370492

YPL 21.339344

ZAHEENSPIN 9.964754

ZAHINTEX 7.858197

ZEALBANGLA 150.338525

Name: Close, Length: 412, dtype: float64

In [ ]:

# 6. Identify the top 5 and bottom 5 stocks based on average closing price

In [36]:

top_5_stocks = average_closing_price.nlargest(5)

bottom_5_stocks = average_closing_price.nsmallest(5)

print("Top 5 Stocks based on Average Closing Price:")

print(top_5_stocks)

print("\nBottom 5 Stocks based on Average Closing Price:")

print(bottom_5_stocks)

Top 5 Stocks based on Average Closing Price: Name APSCLBOND 5413.238636 RECKITTBEN 5342.024793 PREBPBOND 4918.357143 IBBL2PBOND 4851.330357 PBLPBOND 4836.195652 Name: Close, dtype: float64 Bottom 5 Stocks based on Average Closing Price: Name FAMILYTEX 4.698361 ICBIBANK 4.725620 FBFIF 5.289344 POPULAR1MF 5.368033 PHPMF1 5.417213 Name: Close, dtype: float64

In [ ]:

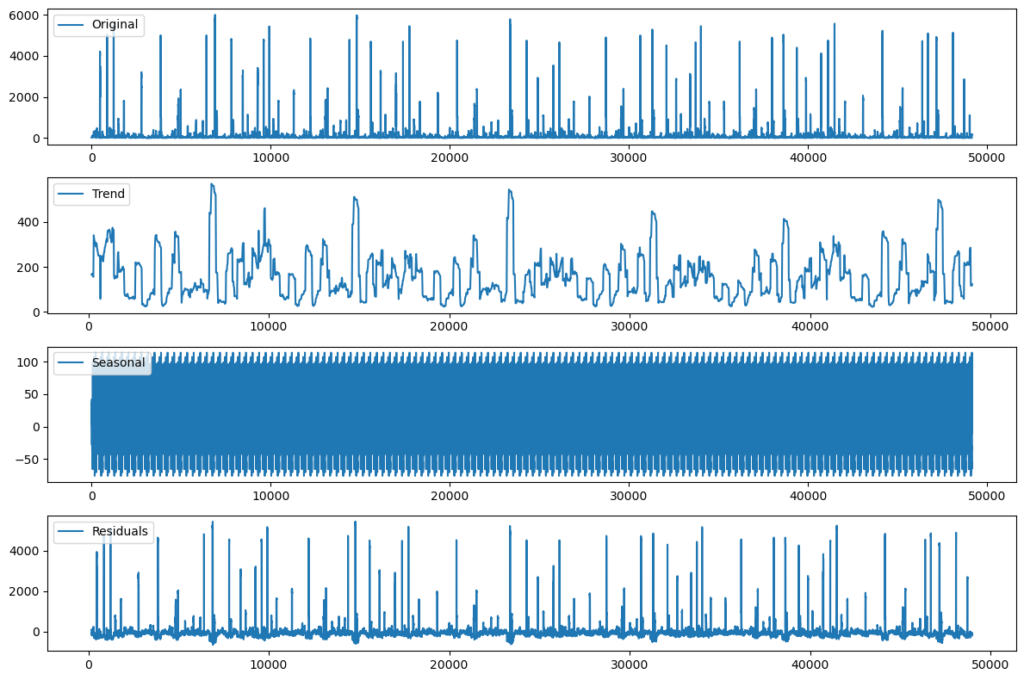

# 3. Investigate the presence of any trends or seasonality whats happen to this one

In [39]:

import statsmodels.api as sm # Perform time series decomposition result = sm.tsa.seasonal_decompose(stock_data['Close'], model='additive', period=365) # Plot the decomposition plt.figure(figsize=(12, 8)) plt.subplot(411) plt.plot(stock_data['Close'], label='Original') plt.legend(loc='upper left') plt.subplot(412) plt.plot(result.trend, label='Trend') plt.legend(loc='upper left') plt.subplot(413) plt.plot(result.seasonal, label='Seasonal') plt.legend(loc='upper left') plt.subplot(414) plt.plot(result.resid, label='Residuals') plt.legend(loc='upper left') plt.tight_layout() plt.show()

In [ ]:

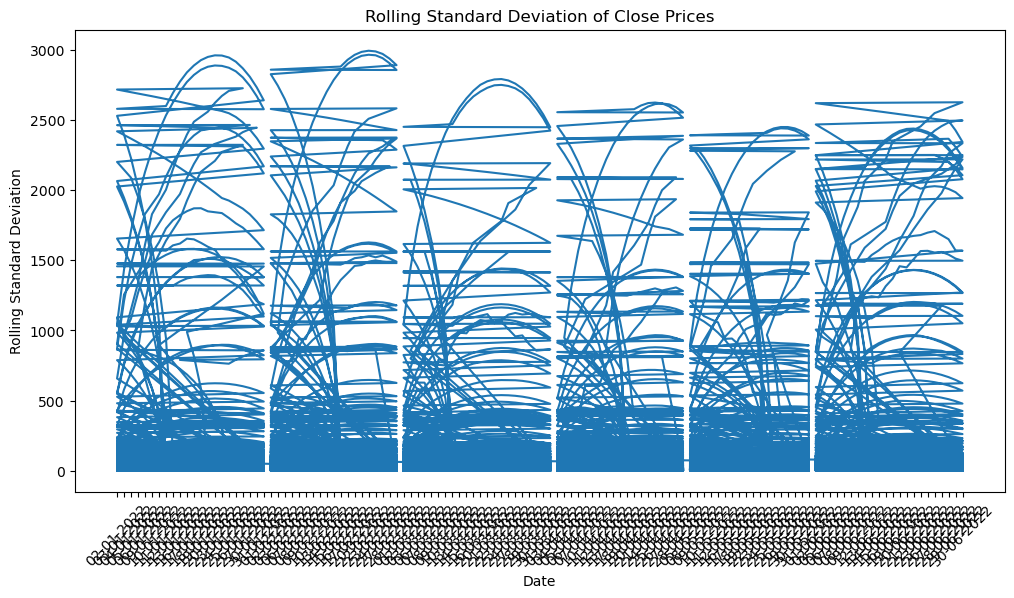

Part-3: Volatility Analysis # 1. Calculate and plot the rolling standard deviation of the 'Close' prices

In [40]:

rolling_std = stock_data['Close'].rolling(window=30).std()

plt.figure(figsize=(12, 6))

plt.plot(stock_data['Date'], rolling_std)

plt.title('Rolling Standard Deviation of Close Prices')

plt.xlabel('Date')

plt.ylabel('Rolling Standard Deviation')

plt.xticks(rotation=45)

plt.show()

In [ ]:

# 2. Create a new column for daily price change (Close - Open)

In [47]:

stock_data['Daily_Price_Change'] = stock_data['Close'] - stock_data['Open']

In [ ]:

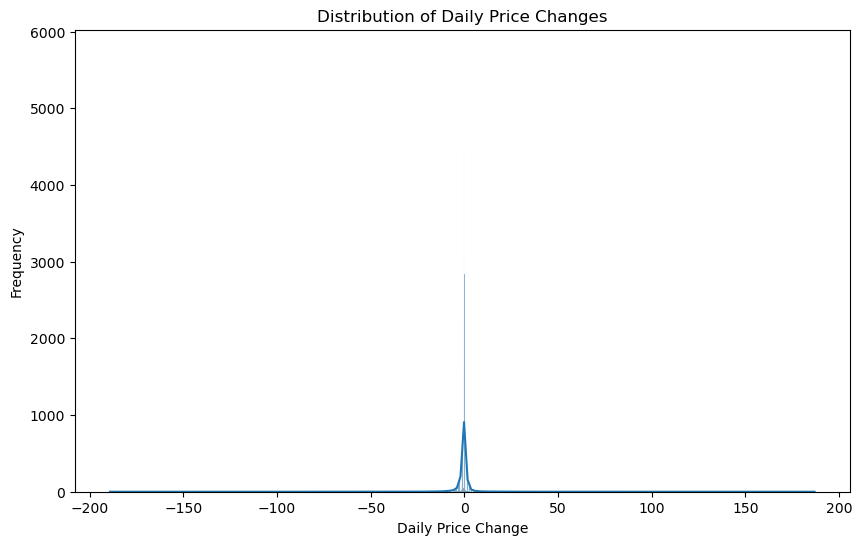

#3. Analyze the distribution of daily price changes

In [48]:

plt.figure(figsize=(10, 6))

sns.histplot(stock_data['Daily_Price_Change'], kde=True)

plt.title('Distribution of Daily Price Changes')

plt.xlabel('Daily Price Change')

plt.ylabel('Frequency')

plt.show()

C:\Users\HP\anaconda3\Lib\site-packages\seaborn\_oldcore.py:1119: FutureWarning: use_inf_as_na option is deprecated and will be removed in a future version. Convert inf values to NaN before operating instead.

with pd.option_context('mode.use_inf_as_na', True):

In [ ]:

#4. Identify days with the largest price increases and decreases

In [49]:

largest_increase = stock_data.nlargest(5, 'Daily_Price_Change')

largest_decrease = stock_data.nsmallest(5, 'Daily_Price_Change')

print("Days with Largest Price Increases:")

print(largest_increase[['Date', 'Daily_Price_Change']])

print("\nDays with Largest Price Decreases:")

print(largest_decrease[['Date', 'Daily_Price_Change']])

Days with Largest Price Increases:

Date Daily_Price_Change

48081 29-06-2022 187.0

46684 27-06-2022 145.5

46681 21-06-2022 141.5

6878 05-01-2022 125.6

44145 30-06-2022 124.5

Days with Largest Price Decreases:

Date Daily_Price_Change

23365 07-03-2022 -189.2

2774 03-01-2022 -182.5

31312 28-04-2022 -178.7

2786 20-01-2022 -166.6

6896 31-01-2022 -154.9

In [ ]:

# 5. Identify stocks with unusually high trading volume on certain days # Define unusually high volume as volume greater than 2 standard deviations from the mean

In [50]:

mean_volume = stock_data['Volume'].mean()

std_volume = stock_data['Volume'].std()

unusual_volume = stock_data[stock_data['Volume'] > (mean_volume + 2 * std_volume)]

print("\nStocks with Unusually High Trading Volume:")

print(unusual_volume[['Date', 'Name', 'Volume']])

Stocks with Unusually High Trading Volume:

Date Name Volume

52 12-01-2022 03.Ceramics_Sector 3148906.60

54 16-01-2022 03.Ceramics_Sector 3351889.00

319 17-01-2022 15.Services_&_Real_Estate 6056375.75

320 18-01-2022 15.Services_&_Real_Estate 5141492.75

321 19-01-2022 15.Services_&_Real_Estate 3928104.25

... ... ... ...

49075 08-06-2022 YPL 4296959.00

49081 16-06-2022 YPL 3394619.00

49089 28-06-2022 YPL 6145142.00

49090 29-06-2022 YPL 4463125.00

49091 30-06-2022 YPL 3844363.00

[1610 rows x 3 columns]

In [ ]:

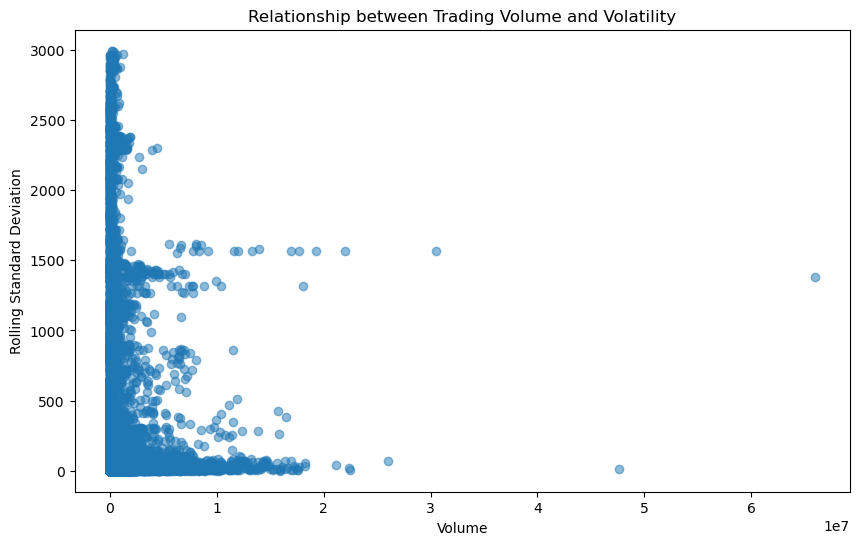

Part 4: Correlation and Heatmaps: #1. Explore the relationship between trading volume and volatility

In [51]:

plt.figure(figsize=(10, 6))

plt.scatter(stock_data['Volume'], rolling_std, alpha=0.5)

plt.title('Relationship between Trading Volume and Volatility')

plt.xlabel('Volume')

plt.ylabel('Rolling Standard Deviation')

plt.show()